Technology ≠ Product ≠ Company. And That's Where Most Ventures Die.

The technology works. You've verified it. You have data. You have proof points. The CTO is convinced. The business unit leader sees the potential.

And then nothing happens.

Or — worse — something does happen. A team assembles. A prototype is built. A market is identified. But somewhere between validation and commercialization, the venture stalls. The technology is solid. The market exists. But the company never fully materializes.

This is the most underrated failure pattern in corporate venture building. It's not the technology that's flawed. It's not the market that disappeared. It's that three completely different disciplines were treated as if they were one.

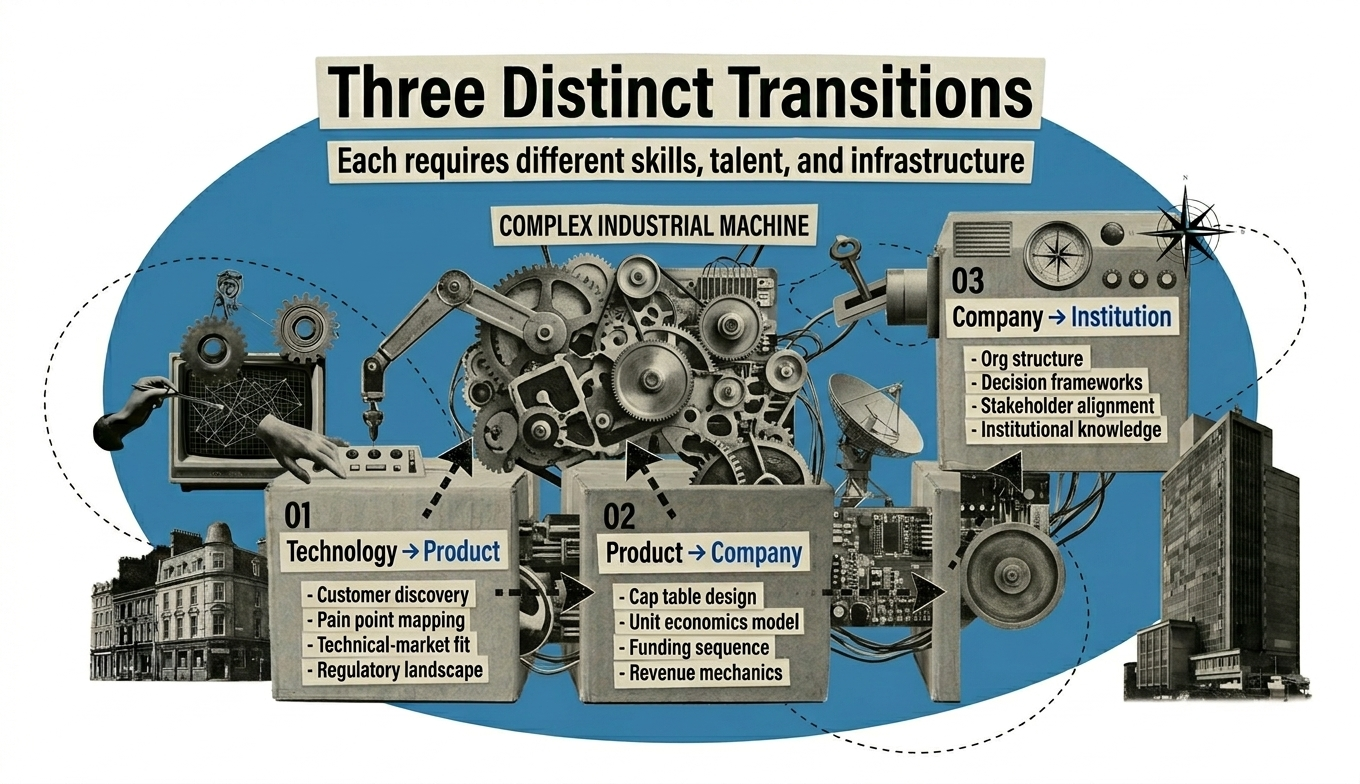

The Three Transitions That Look Like One

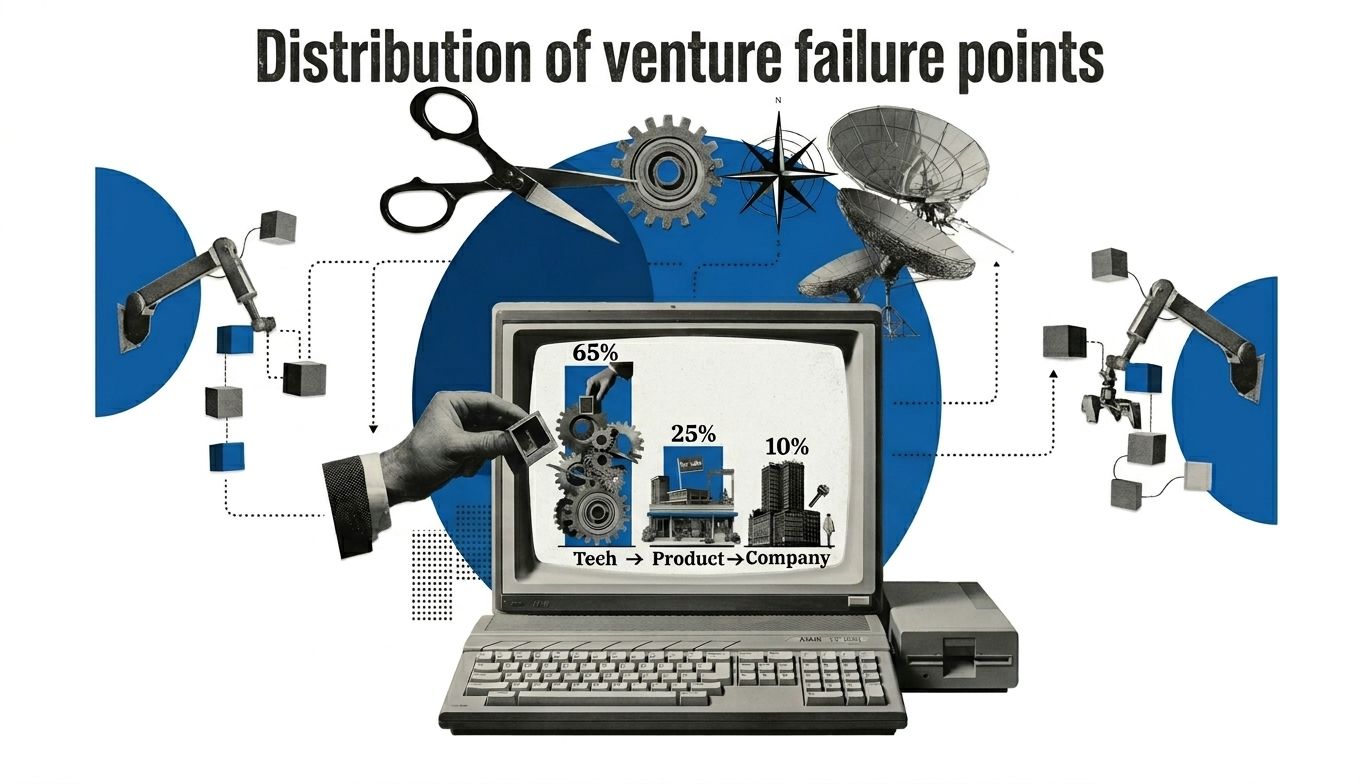

This is the core argument I made in the first article of this series' predecessor: 95% of patents never become companies. But that's only half the story. Because when someone does step in to build — when a corporate decides to take execution responsibility — the failure often doesn't disappear. It shifts. The infrastructure gap that kills academic spinouts is different from the infrastructure gap that kills corporate ventures. But the fundamental problem remains the same.

Technology, product, and company are three completely separate domains. Each has its own disciplines. Each requires different skills. And failure at any one of them, at any stage, kills the venture.

Let me separate them:

Transition 1: Technology to Product

A technology is a capability. It solves a problem, but usually, it solves it in a specific way, for a specific context, at a specific scale.

Moving from "the technology works" to "the product works" requires translation. Market translation.

You need to know:

- Where does this technology create measurable customer value?

- What problem is it actually solving, relative to what exists today?

- At what scale does it work? (A battery technology that works brilliantly at 100g may be worthless at 1kg.)

- What's the minimum viable technical capability? (Most R&D teams want to perfect the technology. Most markets want it "good enough" at a price they'll pay.)

- What trade-offs must you make to commercialize it? (Speed vs. cost, flexibility vs. durability, upfront investment vs. operating expense.)

The technology discipline is "Can we build it?" The product discipline is "Will customers pay for it?"

These are not the same question.

"The technology discipline is 'Can we build it?' The product discipline is 'Will customers pay for it?' These are not the same question."

In deep tech, this transition is where many ventures stumble. An advanced materials company develops a superior composite. In lab conditions, it outperforms existing solutions by 40%. But at commercial scale, the manufacturing process costs 3x more than the current market leader charges. The technology works. The product doesn't. Not yet, anyway — and discovering this after you've invested €5M in a pilot facility is expensive.

Transition 2: Product to Company

Now assume you've solved that. You have a product that customers want and will pay for.

Building a company around that product requires an entirely different set of disciplines:

- Team design — the product works because the original development team understood it intimately. Can you scale decision-making beyond that initial team?

- Financial architecture — unit economics, capital efficiency, pricing strategy, cash flow management, break-even roadmap.

- Governance structure — who decides what, by what process, with what authority?

- Stakeholder architecture — the product may have been built for one decision-maker (the CTO, the business unit head, the innovation officer). A company must satisfy multiple stakeholders with conflicting incentives.

- Capital structure — how capital flows into the venture, how risk is shared, how the exit works.

- Operational rhythm — how decisions are made, how progress is measured, how problems are escalated and solved.

A strong product can be terrible company architecture. You can have the best product in the market and still fail because the team can't execute, the cap table is broken, the financial model doesn't work, or the internal stakeholders aren't aligned.

"You can have the best product in the market and still fail because the team can't execute, the cap table is broken, the financial model doesn't work, or the internal stakeholders aren't aligned."

I've seen both. I've built both. And I can tell you: they're different problems.

The Compounding Nature of the Gaps

In software, these transitions are relatively quick. A prototype can test product-market fit in weeks. A company structure can be adjusted rapidly. Capital requirements are usually manageable.

In deep tech — materials, hardware, biotech, advanced manufacturing — each transition has longer timelines and higher costs. A wrong decision at the technology-to-product transition can cost millions in facilities, equipment, and regulatory navigation. A wrong decision at the product-to-company transition can mean years of restructuring before you can raise institutional capital.

This is why sequencing matters so much in deep tech. But sequencing is only meaningful if you acknowledge that each transition requires fundamentally different expertise.

Where This Fails in Corporates

Corporate ventures encounter these gaps with particular force. Here's why:

The technology already exists — it's internal R&D, or it's sourced from a partner institution. There's no ambiguity about the first step. Someone has already taken responsibility for the technology.

But the translation from "we have this technology" to "this could be a business" usually lands on whichever executive had the conviction to push for the venture in the first place. Often, this is the CTO, the Head of Innovation, or a visionary business unit leader.

That person understands one transition well. Rarely do they understand all three.

The CTO deeply understands the technology. She may not understand market translation or financial architecture.

The innovation officer understands the business case and can build investor narratives. He may not understand the technical de-risking required or the team architecture that turns product into operation.

The business unit leader understands the market and the customer. She may not understand venture governance or how to scale decision-making across a new team.

As long as the venture stays small and internal, this misalignment is hidden. But as soon as the corporate needs to commit real capital — as soon as the venture reaches a funding gate, or needs to hand the business off to an operating team — the gaps become visible. Often, they're visible too late to fix cleanly.

What Actually Happens in Practice

In one real example I worked through:

A large industrial corporation had developed a promising sensor technology for condition monitoring. The technology was solid. The market was real — predictive maintenance is a known pain point. The business unit leader was convinced. An internal team was assembled.

Within six months, they had a prototype. Within nine months, they had first customers. At month twelve, they realized the product-to-company transition had never happened.

The CTO had led technology selection. The business unit leader had identified customers. But no one had designed the founding team. No one had built the financial model. No one had created governance structures that worked outside the corporate hierarchy. When it came time to hire a CEO and transition to independent operation, the company had no cap table, no clear decision-making authority, and no operating rhythm outside the corporate approval process.

The venture didn't fail because the technology failed or the market failed. It failed because nobody owned all three transitions as a single, integrated build. Each transition was handled by a different internal function — and none of them had the mandate or the skills to build a company from scratch.

What This Means for Venture Building

If you're building ventures inside or alongside a corporation, you need to treat each transition as a discrete design problem:

Transition 1 — Technology to Product:

This is about market translation. Who has the highest-value pain point? How does this technology solve it better than alternatives? What's the minimum viable technical capability? You need people fluent in both technology and market, not one or the other.

Transition 2 — Product to Company:

This is about architecture. It includes team design, financial model construction, governance structure, and capital architecture. This is engineering, not creativity. It's as technical as the technology itself, and it's where most ventures break down.

Transition 3 — Company to Scale:

This is about operational infrastructure — hiring, processes, delegation, handover from builder to operator. It's the transition from build mode to sustainable business.

Each of these transitions is learnable. Each has patterns. Each has a set of disciplines that separate ventures that make it from ventures that don't.

But they are not interchangeable, and treating them as if they are is how you end up with a technology that works, a product that sells, and still no company.

"Technology that works, product that sells, and still no company — that's the venture building failure mode everyone misses."

Here's the uncomfortable truth for corporate innovation teams: all three transitions require skills that don't exist inside the corporate. The CTO can lead Transition 1. Nobody in the organization is equipped for Transition 2 — because building a company from scratch is not what established organizations do. And Transition 3 fails when the corporate tries to absorb the venture back into its own operating rhythm too early.

The ventures that survive are the ones where someone takes end-to-end execution responsibility for all three transitions — not as an advisor, not as a consultant, but as the builder who owns the outcome. That means building the venture outside the corporate's operating structure, with the corporate's strategic oversight but not the corporate's day-to-day involvement.

It adds discipline. It adds structural separation. But it's the difference between a patent that never becomes a company and a venture that makes it to scale.

Sources

CB Insights - Why Startups Fail: Top 9 Reasons

Harvard Business Review - What Leaders Get Wrong About Strategic Alignment

We don't just write about it. We build it.

Most companies don't fail on ideas — they fail on implementation. We partner with teams to turn methods like this into concrete outcomes: clearer choices, faster delivery, measurable impact.